Break even point (BEP) refers to the activity level at which total revenue equals total cost. Contribution margin is the variable expenses plus some part of fixed costs which is covered. Thus, CM is the variable expense plus profit which will incur if any activity takes place over and above BEP.

- When comparing the two statements, take note of what changed and what remained the same from April to May.

- Thus, CM is the variable expense plus profit which will incur if any activity takes place over and above BEP.

- NFPs apply different accounting pronouncements to contributions and exchanges.

- A high Contribution Margin Ratio indicates that each sale produces more profit than it did before and that the business will have an easier time making up fixed costs.

Get in Touch With a Financial Advisor

Gross margin encompasses all costs of a specific product, while contribution margin encompasses only the variable costs of a good. While gross profit is more useful in identifying whether a product is profitable, contribution margin can be used to determine when a company will break even or how well it covers fixed costs. To understand how profitable a business is, many leaders look at profit margin, which measures the total amount by which revenue from sales exceeds costs. To calculate this figure, you start by looking at a traditional income statement and recategorizing all costs as fixed or variable. This is not as straightforward as it sounds, because it’s not always clear which costs fall into each category. Analyzing the contribution margin helps managers make several types of decisions, from whether to add or subtract a product line to how to price a product or service to how to structure sales commissions.

Fixed Cost vs. Variable Cost

The contribution margin ratio is calculated as (Revenue – Variable Costs) / Revenue. Alternatively, the company can also try finding ways to improve revenues. However, this strategy could ultimately backfire, and hurt profits if customers are unwilling to pay the higher price. The contribution concept is usually referred to as contribution margin, which is the residual amount divided by revenues. It is easier to evaluate contribution on a percentage basis, to see if there are changes in the proportion of contribution to revenues over time. The contribution margin is calculated at both the unit level and the overall level.

Basic Concepts

In addition, although fixed costs are riskier because they exist regardless of the sales level, once those fixed costs are met, profits grow. All of these new trends result in changes in the composition of fixed and variable costs for a company and it is this composition that helps determine a company’s profit. The difference between fixed and variable costs has to do with their correlation to the production levels of a company.

Variable costs tend to represent expenses such as materials, shipping, and marketing, Companies can reduce these costs by identifying alternatives, such as using cheaper materials or alternative shipping providers. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute contribution definition in accounting for consultation with professional advisors. The absence of any indication of a barrier supports the conclusion that the contribution has no donor-imposed conditions. This pledge meets the definition of a contribution in that it is an unconditional transfer of cash that is both voluntary and nonreciprocal. By definition, any societal benefit received by Alpha is not considered to be of commensurate value.

My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. This metric is typically used to calculate the break even point of a production process and set the pricing of a product. They also use this to forecast the profits of the budgeted production numbers after the prices have been set. A low margin typically means that the company, product line, or department isn’t that profitable. An increase like this will have rippling effects as production increases.

A common outcome of contribution analysis is an increased understanding of the number of units of product that must be sold in order to support an incremental increase in fixed costs. This knowledge can be used to drive down fixed costs or increase the contribution margin on product sales, thereby fine-tuning profits. Break-even point (BEP) depends on whether we are discussing the number of units required, or total revenues required to cover total costs.

Company XYZ receives $10,000 in revenue for each widget it produces, while variable costs for the widget are $6,000. The contribution margin is calculated by subtracting variable costs from revenue, then dividing the result by revenue, or (revenue – variable costs) / revenue. Thus, the contribution margin is 40%, or ($10,000 – $6,000) / $10,000. Alternatively, companies that rely on shipping and delivery companies that use driverless technology may be faced with an increase in transportation or shipping costs (variable costs). These costs may be higher because technology is often more expensive when it is new than it will be in the future, when it is easier and more cost effective to produce and also more accessible. A good example of the change in cost of a new technological innovation over time is the personal computer, which was very expensive when it was first developed but has decreased in cost significantly since that time.

Every year, the network holds an advocacy event that includes performances by major entertainers. This event generates contributions and sponsorships by major corporations. ABC engaged in the following transactions during the year ending December 31, 2019.

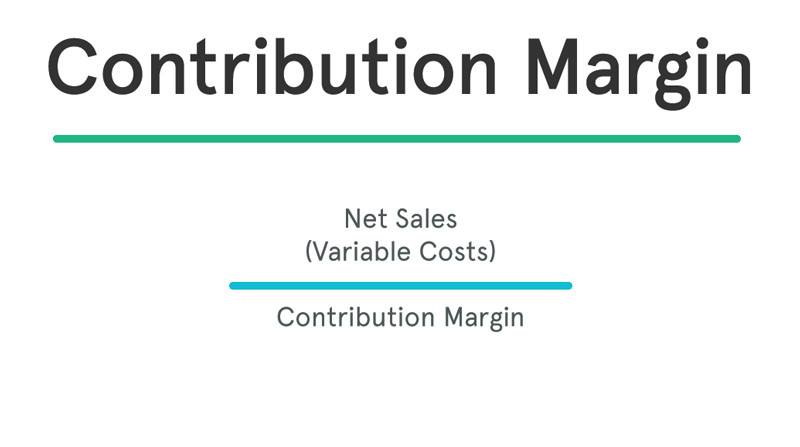

Although the company has less residual profit per unit after all variable costs are incurred, these companies may have little to no fixed costs. The contribution margin formula is calculated by subtracting total variable costs from net sales revenue. A contribution margin ratio of 40% means that 40% of the revenue earned by Company X is available for the recovery of fixed costs and to contribute to profit.